Social Security: How to Maximize Your Retirement Benefits

Investing Roth IRA 401k 403b savings DebtWhen it comes to Social Security, most people know that delaying benefits can increase their monthly checks. But fewer understand the other strategies available—especially those tied to marital status. Making the right decisions can significantly impact your lifetime income, and the earlier you understand your options, the more flexibility you have.

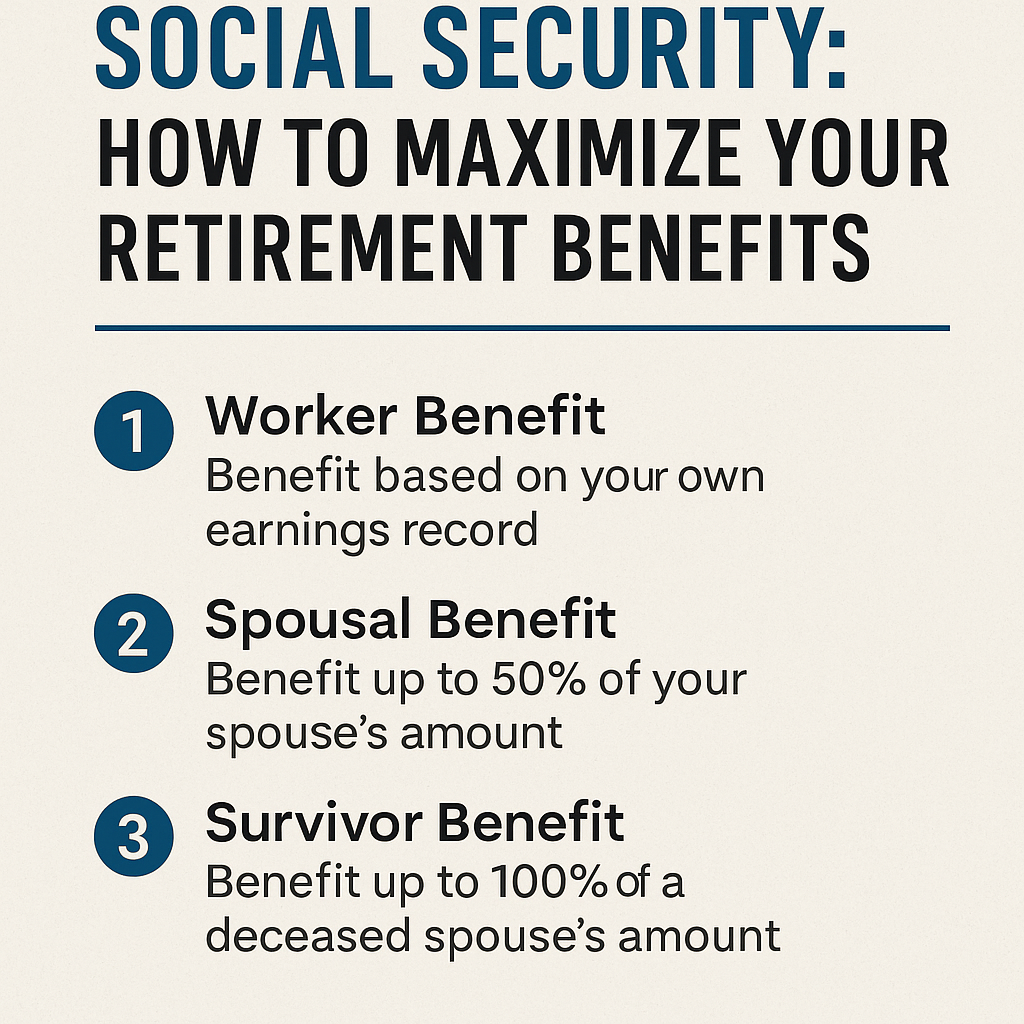

Before diving into strategy, it helps to understand the three types of Social Security retirement benefits:

1. Worker Benefit

This is the benefit you receive based on your own earnings history. You qualify after 40 quarters (10 years) of work. The amount is determined by your highest 35 years of indexed earnings.

2. Spousal Benefit

This benefit is available to married individuals.

- For non-working spouses: up to 50% of the working spouse’s benefit.

- For working spouses: the greater of their own worker benefit or up to 50% of their spouse’s benefit.

3. Survivor Benefit

If your spouse passes away, the surviving spouse may receive:

- Up to 100% of the deceased spouse’s benefit

- Or their own benefit, whichever is higher Survivor benefits can begin as early as age 60 (or earlier in certain cases).

The Most Common Strategy: Delaying Benefits to Age 70

The simplest and often most effective way to maximize your monthly Social Security benefit is by waiting until age 70 to claim. Doing so can increase payments by up to 24% compared to claiming at full retirement age, not including future cost-of-living adjustments.

But for widows, widowers, and those with dual eligibility, there are additional opportunities.

Strategies for Widows and Widowers

Surviving spouses have unique planning opportunities due to the difference between spousal benefits and survivor benefits. Unlike spousal benefits (which max out at 50%), survivor benefits can equal 100% of the deceased spouse’s benefit.

Here are a few powerful strategies:

Strategy 1: Claim the Higher Benefit

If you're eligible for both a worker benefit and a survivor benefit, you can choose the higher of the two. This provides immediate maximization.

Strategy 2: Start Your Own Benefit Early, Switch Later

A widowed spouse may:

- Start their own worker benefit at age 62, then

- Switch to the survivor benefit at full retirement age

This can make sense when the deceased spouse had the larger benefit. Since survivor benefits don’t grow after full retirement age, there is no advantage to delaying them beyond that point.

Strategy 3: Start Survivor Benefits Early, Switch to Your Own Later

A surviving spouse may:

- Begin survivor benefits at age 60, then

- Switch to their own worker benefit at age 70, maximizing delayed retirement credits

This can create a strong income bridge while your own benefit continues to grow toward its maximum.

Why It Matters

Social Security may be the most important income foundation in retirement. Choosing the wrong strategy even by accident can cost tens of thousands of dollars over your lifetime. These rules can be confusing, especially when coordinating multiple benefits, ages, and income sources.

The good news? You don’t have to navigate this alone.

Next Steps

If you want to make sure you’re maximizing every dollar of your Social Security benefits, schedule a Social Security Strategy Session with me.

We’ll:

- Review your earnings history

- Explore all benefit combinations

- Compare claiming ages

- Map out the strategy that provides the greatest lifetime income

Social Security is too valuable to guess your way through it.

👉 Reach out today and let’s build a personalized strategy for your retirement.