The Truth About Roth Conversions: Are They Right for You?

If you have spent any time researching retirement planning, you have almost certainly come across the term "Roth conversion." It gets mentioned frequently, often breathlessly, as a strategy that can save retirees enormous amounts in taxes over their lifetime. That reputation is well earned. But what often gets left out of the conversation is just as important: a Roth conversion is not right for everyone, the timing matters enormously, and done incorrectly it can create a tax bill that does far more harm than good.

This article is a plain-language guide to what Roth conversions actually are, who they tend to benefit most, when to do them, and the mistakes that can turn a smart strategy into a costly one.

Traditional vs. Roth: a quick refresher

Before getting into conversions, it helps to understand the core difference between the two account types, because everything else flows from this distinction.

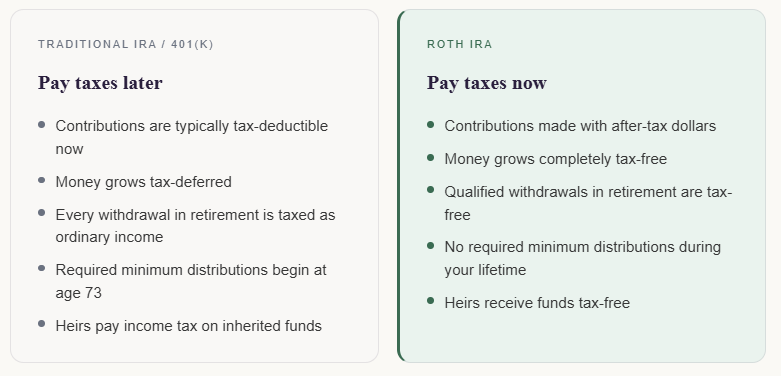

A Roth conversion is simply the act of moving money from a traditional IRA or 401(k) into a Roth IRA. The amount you convert is added to your taxable income for that year, and you pay ordinary income tax on it. In exchange, that money and all its future growth becomes permanently tax-free.

The core question is always the same: is it better to pay the tax now, or later? The answer depends on whether your tax rate today is lower, higher, or the same as it will be in retirement.

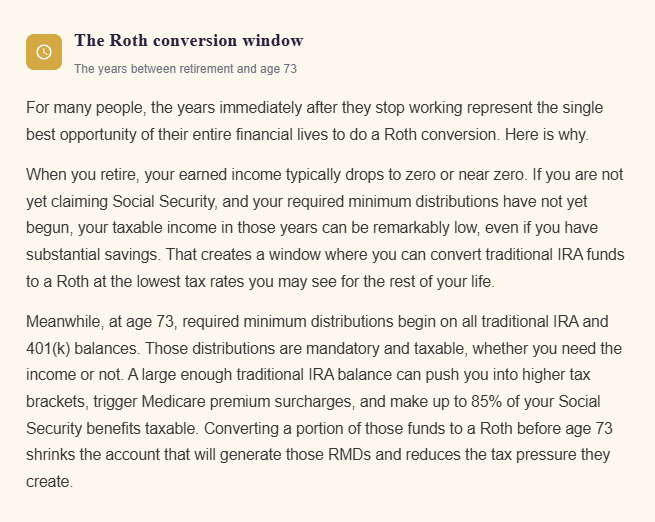

Why the window between retirement and age 73 is so valuable

How to think about which tax bracket to fill

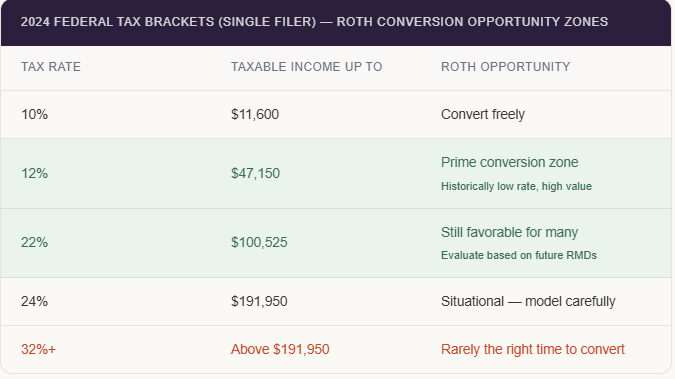

The goal of a Roth conversion strategy is not to convert as much as possible. It is to convert the right amount each year, which usually means filling up a lower tax bracket without crossing into a higher one.

For married couples filing jointly, these bracket thresholds are roughly double. The practical approach is to calculate your projected taxable income for the year from all sources, determine how much room remains before the next bracket threshold, and convert up to that amount. Repeat annually through the window years.

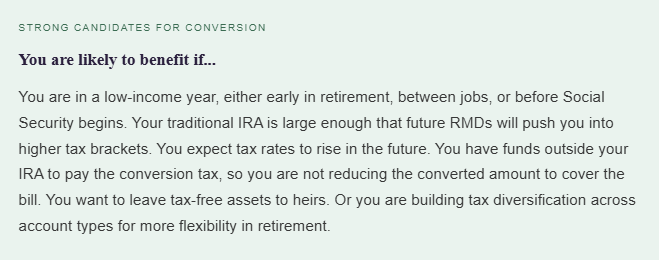

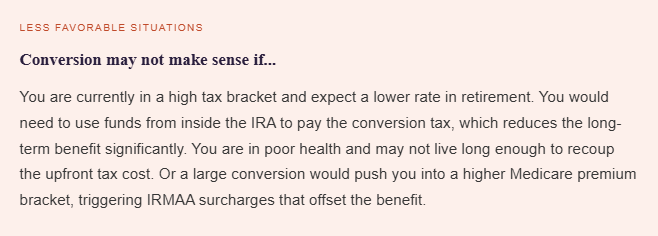

Who benefits most from a Roth conversion

Roth conversions are not universally beneficial. They work best in specific situations.

"A Roth conversion is not a tax elimination strategy. It is a tax timing strategy. The goal is to pay taxes when the rate is lowest, not to avoid them altogether."

The Medicare premium trap most people miss

One of the most overlooked consequences of a large Roth conversion is its effect on Medicare premiums. Medicare Part B and Part D premiums are determined by your income from two years prior. If a conversion bumps your income above certain thresholds, you may face Income-Related Monthly Adjustment Amounts, known as IRMAA surcharges, that can add hundreds of dollars per month to your Medicare costs.

In 2024, IRMAA surcharges begin at $103,000 of modified adjusted gross income for a single filer and $206,000 for a married couple filing jointly. These thresholds are tiered, meaning each jump in income triggers a higher surcharge. A conversion that looks efficient on paper can look considerably different once Medicare premium impacts are factored in.

How to approach a Roth conversion strategy

1. Project your retirement income picture

Start with a clear view of what your taxable income will look like each year between now and age 73, including Social Security, any part-time income, RMDs from existing accounts and any other sources.

2. Identify your conversion window

Determine which years offer the lowest tax rates and the most room in lower brackets. For many people this is the gap between retirement and age 70 when Social Security begins, and before age 73 when RMDs kick in.

3. Model the conversion amount annually

Each year, calculate your projected income from all sources and determine how much you can convert while staying within your target tax bracket. Factor in IRMAA thresholds if you are approaching Medicare age.

4. Pay the tax from outside the IRA

Whenever possible, pay the income tax generated by the conversion from a taxable savings account rather than from the IRA itself. Using IRA funds to cover the tax reduces the amount that ends up in your Roth and significantly diminishes the long-term benefit.

5. Review and adjust every year

Tax laws change, account balances shift, and life circumstances evolve. A conversion strategy that made sense at 63 may look different at 67. Annual reviews with a CFP keep the strategy calibrated to your actual situation.

Done well, a multi-year Roth conversion strategy can reduce lifetime taxes by tens of thousands of dollars, lower future RMD burdens, reduce Medicare premium exposure, and leave a meaningfully larger tax-free legacy to the people you care about. It is one of the most valuable planning conversations a pre-retiree can have, and one of the most underutilized.

The most important thing is not to wait until you are already in retirement to think about it. The earlier in the window you begin, the more years of tax-free growth compound in your favor.