The Sandwich Generation: Caught Between College Costs and Retirement Savings

There is a season of life that financial planners talk about often and that gets far too little attention in the broader conversation about money. It is the decade or so, usually somewhere between your mid-40s and late 50s, when you find yourself financially responsible for people on both sides of you at the same time.

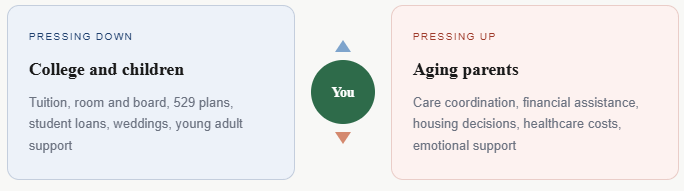

Your kids are approaching college age, and the tuition bills are staggering. Your parents are aging, and they may need financial or caregiving support you did not fully anticipate. And somewhere in the middle of all of that, you are supposed to be building the retirement savings that will carry you through the next 30 years of your own life.

This is the Sandwich Generation. And if you are in it right now, you already know that the financial pressure it creates is unlike anything else you have navigated before.

The numbers behind this season of life are significant. According to Pew Research, roughly half of adults in their 40s and 50s have at least one parent age 65 or older while also either raising a child or supporting an adult child financially. More than one in four Americans in this age group have provided financial support to both a parent and a child in the past year.

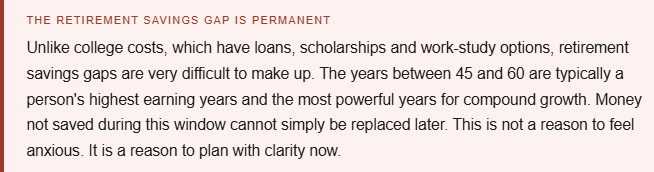

The financial consequences compound quickly. Money flowing out in multiple directions at once is money not flowing into retirement savings, not paying down debt, and not building the kind of financial cushion that makes the next chapter of life feel secure rather than stressful.

The most important rule most people get backwards

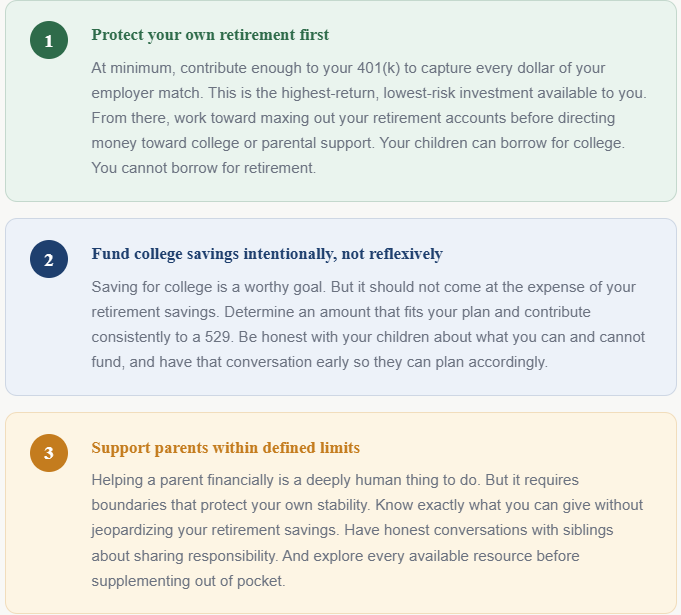

When you are in the middle of the sandwich squeeze, the instinct is to take care of everyone else first and figure out your own situation later. That instinct is understandable. It is also one of the most financially costly mistakes a person in this season of life can make.

There is a reason the airline safety instruction tells you to put on your own oxygen mask before helping others. You cannot sustain support for the people who depend on you if you have depleted your own resources to the point where you need help yourself. The financial version of that principle applies directly here.

"I have never had a client regret saving too much for retirement. I have had many regret not saving enough because they spent those peak earning years funding everyone else's needs first."

The college funding conversation most families avoid

One of the most common dynamics I see in sandwich generation families is a complete absence of honest conversation about what college actually costs and who is actually paying for it. Parents feel guilty about not being able to fully fund their child's education. Children assume more will be covered than actually will be. And the gap gets filled with debt on both sides.

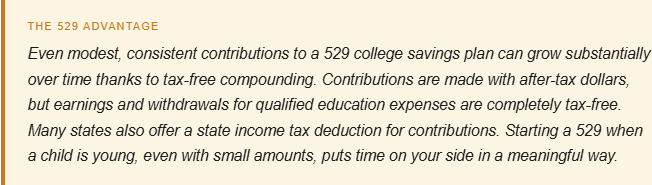

The earlier you can have a clear, numbers-based conversation with your children about college funding, the better. This does not mean telling them their dreams are not achievable. It means giving them accurate information early enough that they can make choices, choose a school that fits the budget, pursue scholarships aggressively, consider community college for the first two years, or take on a manageable amount of student loans with a realistic repayment plan.

A child who graduates with $30,000 in student loans and a degree that leads to employment is in a vastly better position than one who graduates with $80,000 in loans from a school that stretched the family budget to its breaking point. Having that conversation early is one of the most loving financial things a parent can do.

What to do when a parent needs financial help

This is the part of the sandwich that tends to arrive without warning. A parent's health changes, a spouse passes away, savings turn out to be insufficient for the life they are living, and suddenly you are fielding a conversation you never fully prepared for.

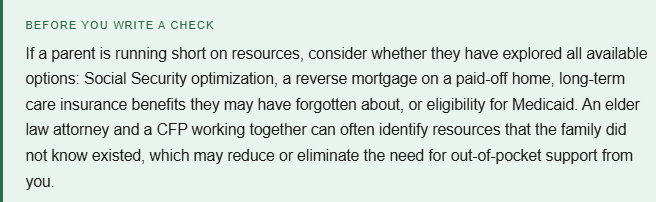

The first step before writing any checks is to get a complete picture of your parent's financial situation. That means understanding their income sources, their assets, their expenses, their insurance coverage, and what government benefits they may be eligible for but not yet receiving. Many families discover that there are resources available, including Medicare benefits, state assistance programs, Veterans Affairs benefits for eligible parents, and nonprofit organizations that provide support, that have not been explored.

If financial support from you is genuinely needed, treat it as a line item in your budget rather than an open-ended commitment. Know the monthly number, make sure it fits within your plan, and have a conversation with any siblings about shared responsibility. Carrying that weight alone when others could participate is one of the most common and most avoidable sources of financial strain in sandwich generation families.

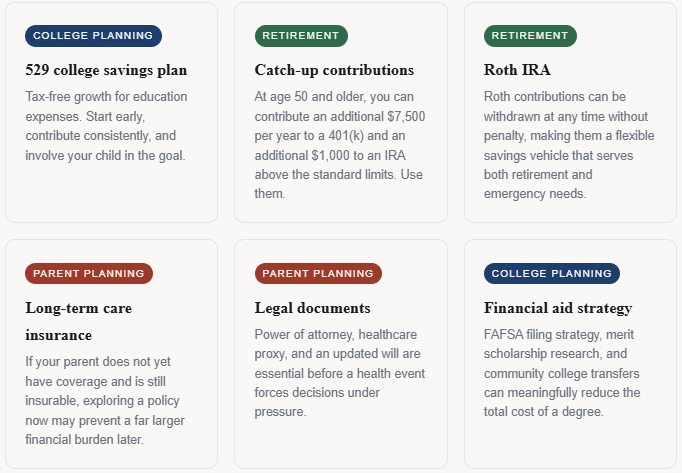

The tools that help in this season

Navigating three competing financial priorities at once is exactly the kind of problem that benefits from a coordinated plan rather than a series of ad hoc decisions. Here are the planning tools that tend to matter most for sandwich generation families.

The emotional weight is real too

It would be incomplete to talk about the Sandwich Generation purely in financial terms. The emotional dimension of this season is just as significant, and it affects financial decisions in ways that are easy to underestimate.

Guilt is the most common feeling I hear described: guilt about not doing enough for a parent, guilt about not being able to fully fund a child's education, guilt about prioritizing your own retirement when others have needs. That guilt, if left unexamined, drives financial decisions that feel emotionally right in the moment and are strategically wrong over the long term.

Giving more than your plan can sustain is not generosity. It is borrowing against your own future security and, ultimately, potentially creating a situation where your children have to support you in the same way you are supporting your parents right now. The most loving financial decision you can make for the people around you is to keep your own financial life on solid ground.

If you are in the middle of the sandwich squeeze right now, the most important thing you can do is get a clear picture of your total financial situation across all three areas, establish a priority order you can actually live with, and build a plan that moves all three forward simultaneously even if imperfectly. Imperfect progress in all three areas beats perfect focus on one while the others collapse.

This is exactly the kind of season where having a financial advisor in your corner makes the most tangible difference. Not because the math is beyond you, but because the emotional complexity of these decisions makes it very hard to think clearly about your own situation when you are in the middle of it.