Retirement Redefined — What It Actually Looks Like Today

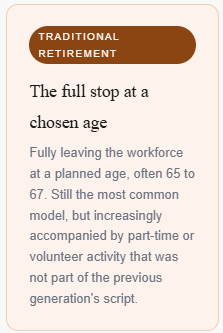

For most of the twentieth century, retirement looked roughly the same for everyone. You worked for decades, collected a pension or a gold watch, and spent your final years in relative quiet. The financial plan that supported this version of retirement was straightforward: save enough to cover your expenses, claim Social Security, and draw down your savings in a predictable line until you no longer needed them.

That model is not gone entirely. But it is no longer the dominant one. The way Americans think about, plan for, and actually live retirement has shifted dramatically over the past two decades, driven by longer lifespans, changing attitudes about work and purpose, improved health in later years, and the practical reality that many people simply do not want to stop doing meaningful things at 65.

If you are planning for retirement using the assumptions of a generation ago, there is a real chance your plan does not match the retirement you actually want to live.

The new shapes of retirement

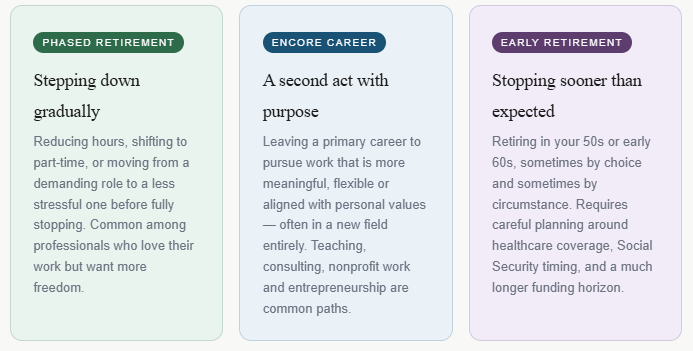

Modern retirement does not follow a single script. It comes in several distinct shapes, each with its own lifestyle and financial implications. Understanding which version resonates with you is the first step toward building a plan that actually fits.

The financial implications of each path are meaningfully different. A phased retirement with part-time income dramatically changes your Social Security timing strategy and your early withdrawal needs. An encore career that generates income for five or ten years can add hundreds of thousands of dollars to lifetime financial security. An early retirement at 58 means potentially 35 years without a paycheck, which is a fundamentally different planning challenge than retiring at 67.

The financial implications of each path are meaningfully different. A phased retirement with part-time income dramatically changes your Social Security timing strategy and your early withdrawal needs. An encore career that generates income for five or ten years can add hundreds of thousands of dollars to lifetime financial security. An early retirement at 58 means potentially 35 years without a paycheck, which is a fundamentally different planning challenge than retiring at 67.

Why longer lives change everything

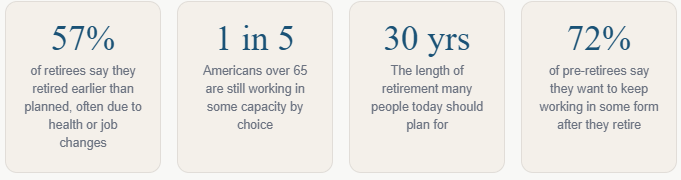

The retirement your grandparents planned for lasted perhaps ten years. The retirement you are planning for could easily last thirty. That is not a minor adjustment. It is a fundamental reimagining of what retirement is and what it requires financially.

A thirty-year retirement has three distinct chapters, which we have written about before using the framework of the Go Go Years, the Slow Go Years and the No Go Years. Early retirement is active, expensive and full of the experiences people spent decades looking forward to. The middle years slow naturally. The final years bring a different set of costs, centered largely on healthcare and care needs.

Planning for a long retirement also means planning for inflation in a way that shorter retirements did not require. A dollar today buys meaningfully less in twenty years. A retirement income plan that does not account for purchasing power erosion will feel comfortable at 67 and strained at 82. Growth-oriented investing does not end at retirement. It simply shifts in proportion and purpose.

The rise of the encore career

One of the most significant shifts in modern retirement is the growing number of people who do not want to stop working entirely. They want to stop doing the work they have been doing in the way they have been doing it. That is a very different thing.

An encore career is a second act that typically brings together professional skills, personal passions and a desire to contribute in a way that feels more aligned with values than a primary career often allowed. A corporate attorney who becomes a mediator. A marketing executive who starts a consulting firm. A teacher who opens a tutoring business. A nurse who becomes a health coach.

The financial impact of an encore career can be substantial even if the income is modest. Someone who generates $40,000 a year in encore career income from age 62 to 72 is not just earning $400,000 over that decade. They are also delaying Social Security to maximize their benefit, leaving their investment portfolio untouched for ten additional years of compounding, and potentially avoiding early Medicare eligibility gaps. The combined financial impact of those three factors can be enormous.

Early retirement — the plan most people underestimate

Early retirement, stopping work in your 50s or very early 60s, has become one of the most searched and discussed topics in personal finance. The appeal is obvious. The reality is more complicated than most of the content about it suggests.

The financial challenges of early retirement are distinct from those of traditional retirement in several important ways. Healthcare coverage is the most immediate. Before Medicare eligibility at 65, you are responsible for your own health insurance, which can cost a family several hundred to well over a thousand dollars per month depending on coverage level and income. That cost needs to be explicitly built into the plan, not assumed away.

Early retirement also means a longer period of portfolio dependence. Someone retiring at 58 with a life expectancy into their late 80s needs their portfolio to last 30 years or more, potentially starting withdrawals earlier than optimal and without the cushion of Social Security income for the first several years. The sequence of returns in those early years is critical. A significant market downturn in the first five years of early retirement can permanently impair a portfolio in ways that are very difficult to recover from.

None of this means early retirement is not achievable. Many people do it successfully with careful planning. But the plan needs to be built around the actual numbers, not an optimistic assumption that it will work out.

What a modern retirement plan actually needs to address

If retirement today is more varied, more personal and longer than it used to be, then the retirement plan needs to be more sophisticated too. A plan built around a single retirement date, a fixed annual withdrawal rate and a standard portfolio mix is not adequate for the range of retirement paths people are actually living.

- A clear picture of what retirement actually looks like for you. What age do you want to stop working fully? Is there an encore career or part-time work in the picture? Where will you live? What does an active year of spending look like versus a quieter one? These answers drive every financial number that follows.

- A phased spending model across all three chapters. Rather than a flat annual budget, a plan that accounts for higher spending in the active years, moderate spending in the transition years and healthcare-dominated costs in the later years reflects how retirement actually unfolds.

- A Social Security strategy calibrated to your actual timeline. When you retire relative to when you claim Social Security has enormous financial consequences. Phased retirement, encore careers and early retirement all change the optimal claiming strategy in ways that a standard plan often misses.

- Healthcare coverage from retirement to Medicare. If you retire before 65, healthcare coverage needs to be explicitly funded. COBRA, marketplace plans and spousal coverage each carry costs and limitations that need to be modeled into the plan.

- A portfolio strategy built for a long runway. A thirty-year retirement requires growth-oriented investing well into retirement, not a conservative posture that cannot keep up with inflation. The portfolio strategy needs to match the actual timeline, not a generic assumption about age-based risk reduction.

- Flexibility built in for the unexpected Modern retirement brings more variables than the traditional model did. Health changes, family needs, encore career income that performs differently than expected, housing decisions that shift — a good plan has enough flexibility to absorb these without requiring a complete rebuild. The most important shift in how we think about retirement planning today is moving from a single destination mindset to a journey mindset. Retirement is not the finish line. It is the start of a chapter that could last as long as your entire working life. It deserves a plan built with that scope in mind.

If your current retirement plan was built around assumptions that no longer match the retirement you actually want to live, that conversation is worth having sooner rather than later. The earlier you align your plan to your vision, the more options you will have to shape both.