Is Your Insurance Still Aligned With Your Life?

There is a pattern I see repeatedly in financial planning reviews that never stops being surprising. A client sits down, we pull up their full financial picture, and somewhere in the insurance section we find a policy they bought fifteen years ago that made complete sense at the time and makes almost no sense now. Or worse, a coverage gap that opened quietly during a life transition and has been sitting there unnoticed ever since.

Insurance is one of those areas of personal finance that people tend to set and forget. You buy a life insurance policy when you have your first child, you sign up for whatever disability coverage your employer offers, and you renew your homeowners policy every year without reading it. Life moves on. The coverage stays exactly where you left it.

The problem is that your life has almost certainly changed significantly since you last thought carefully about your insurance. Your income is different. Your family situation has evolved. Your mortgage balance has shifted. Your net worth has grown. Your parents may now depend on you. Your children may no longer depend on you. Every one of those changes has implications for whether your coverage is still doing the job it was designed to do.

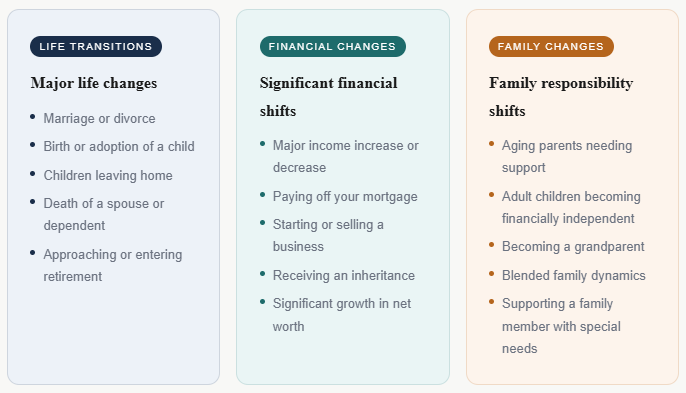

When life changes, insurance needs change too

There is no single moment when your insurance review is due. But there are specific life events that almost always signal that your coverage deserves a fresh look. If any of these sound familiar, it may be time to sit down and evaluate where you stand. Even without a specific triggering event, a general rule worth following is to do a meaningful insurance review every three to five years. The world changes, your life changes, and coverage that felt adequate becomes inadequate so gradually that it is easy to miss.

Even without a specific triggering event, a general rule worth following is to do a meaningful insurance review every three to five years. The world changes, your life changes, and coverage that felt adequate becomes inadequate so gradually that it is easy to miss.

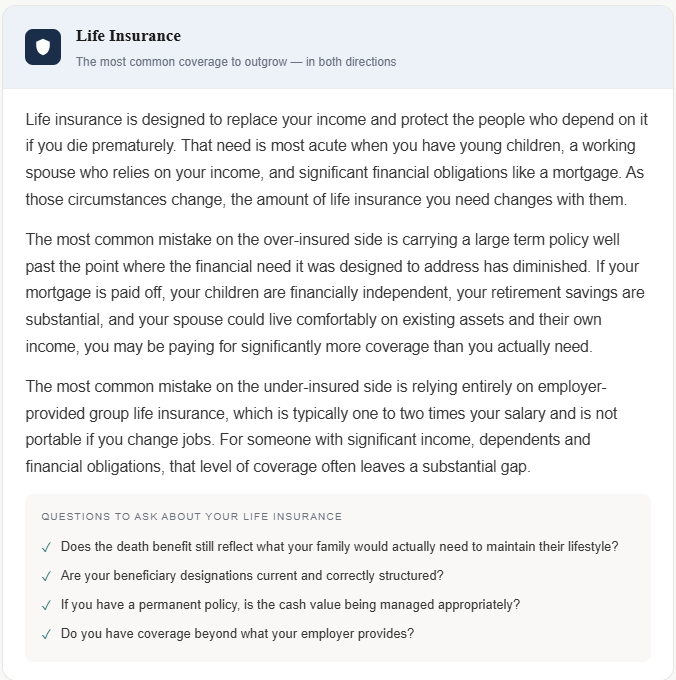

Life insurance: the coverage most people get wrong twice

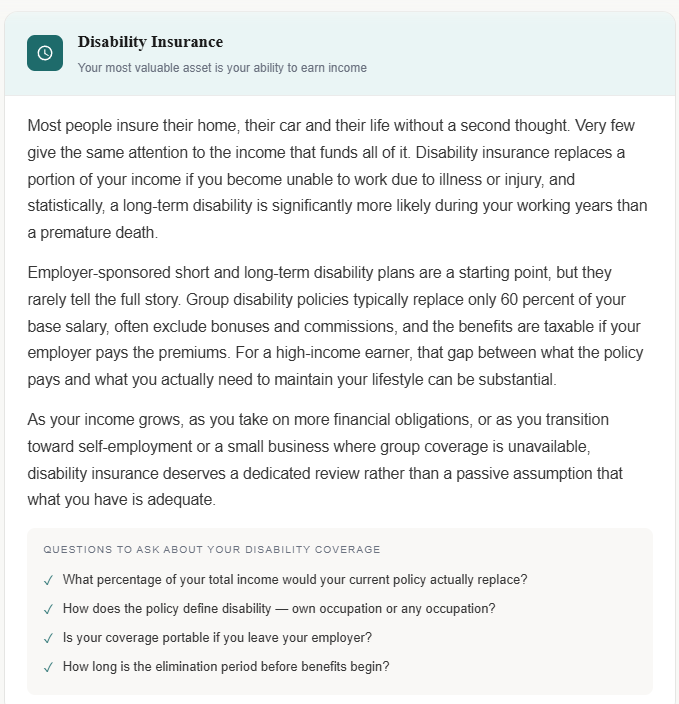

Disability insurance: the most overlooked protection you have

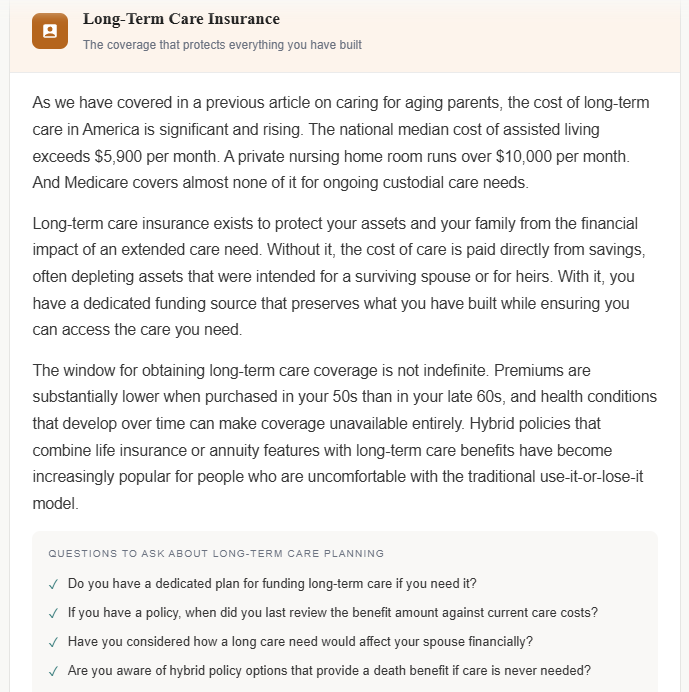

Long-term care insurance: planning for the chapter most people ignore

investor.genworth.com/news-events/press-releases/detail/982/genworth-and-carescout-release-cost-of-care-survey-results

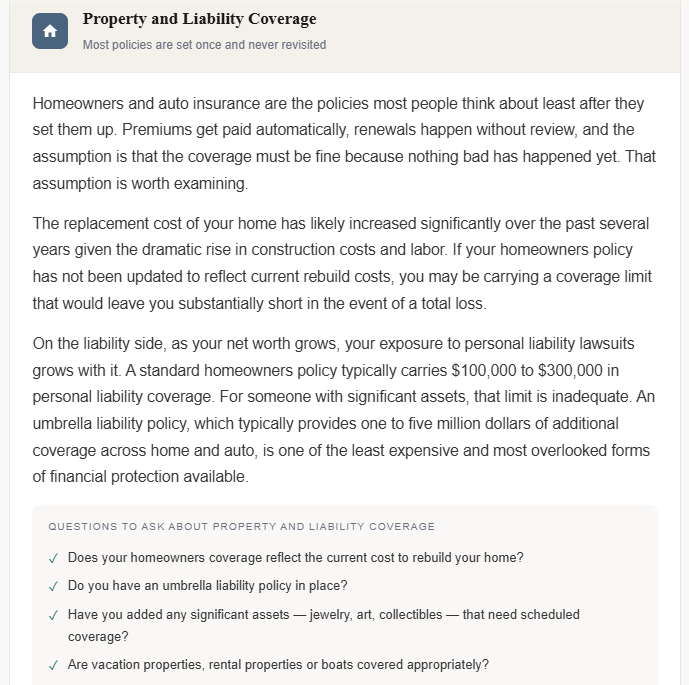

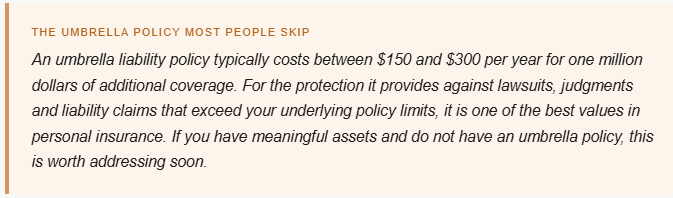

Property and liability: the coverage that grows with your net worth

The empty nest insurance reset

One of the most significant insurance review moments that goes overlooked is when the last child leaves home. The financial landscape of your life shifts meaningfully at that point, and your insurance coverage often has not caught up.

Life insurance needs typically decrease when children become financially independent, your mortgage balance has declined significantly, and two incomes have had years to build retirement savings. Paying the same premium for the same coverage as when you had three dependents and a new mortgage is worth reconsidering.

At the same time, the conversation about long-term care insurance becomes more urgent as you move through your 50s and toward retirement. The window for getting coverage at a reasonable cost narrows with each passing year. The empty nest years, when cash flow often improves significantly, are frequently the right moment to have that conversation seriously.

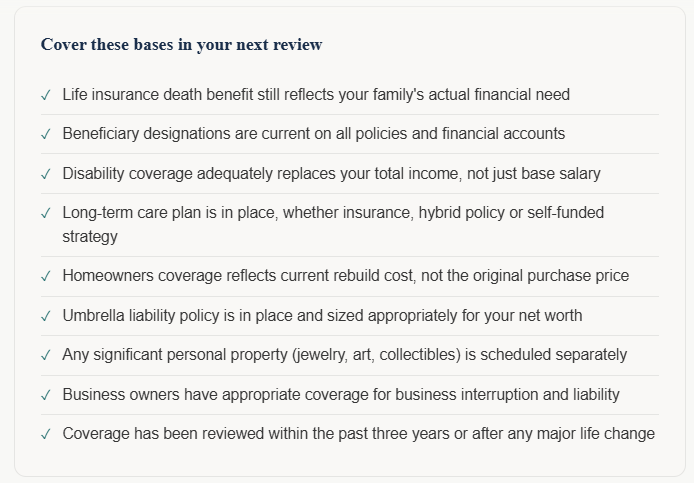

Your insurance review checklist

Insurance is not the most exciting part of financial planning. But it is the foundation that everything else sits on. A well-built investment portfolio and a carefully constructed retirement plan can be significantly disrupted by a coverage gap that surfaces at exactly the wrong moment. Getting this part right does not take much time. It just takes the intention to actually look.