How to Create a Paycheck in Retirement

There is a moment that nearly every new retiree describes the same way. It is the morning of the first month after they stop working, and they realize that no paycheck is coming. They know this intellectually. They have planned for it. But the feeling of it the absence of that automatic deposit that has shown up reliably for 30 or 40 years is something different entirely.

Creating your own income in retirement is one of the most complex financial challenges most people will ever face. It is not just about having enough saved. It is about converting what you have saved into a reliable, sustainable stream of income that covers your expenses, keeps up with inflation, minimizes your tax bill, and lasts for a retirement that could easily span 25 to 30 years.

The good news is that this problem is very solvable. But it requires a plan that goes well beyond simply deciding what percentage of your portfolio to withdraw each year.

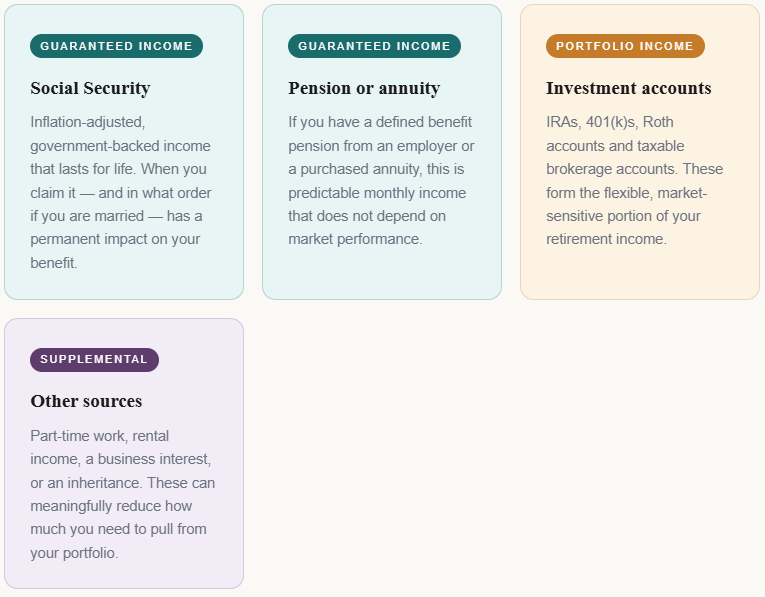

Start with what you already have

Before you think about how to draw from your savings, you need a clear picture of the guaranteed income sources that will form the foundation of your retirement paycheck. For most people, this means two things: Social Security and any pension or annuity income they may have.

The gap between your guaranteed income and your actual monthly expenses is the number that your portfolio needs to fill. That gap is your starting point for building a withdrawal strategy.

The sequence of withdrawals matters more than you think

Once you know your income gap, the next question is which accounts you draw from first. This is where a lot of retirees leave significant money on the table, not because they run out of savings, but because they draw down their accounts in the wrong order and create unnecessary tax burdens along the way.

The general framework most financial advisors use is to draw from taxable accounts first, then tax-deferred accounts like traditional IRAs and 401(k)s, and finally Roth accounts. But like most general rules, this one has important exceptions depending on your specific situation.

1. Taxable brokerage accounts first

Drawing from taxable accounts early allows your tax-advantaged accounts to continue growing. Long-term capital gains in taxable accounts are also taxed at lower rates than ordinary income, making this an efficient first source.

2. Tax-deferred accounts next

Traditional IRAs and 401(k)s are taxed as ordinary income when you withdraw. Drawing these down before age 73 also reduces the size of future required minimum distributions, which can otherwise push you into higher tax brackets later.

3. Roth accounts last

Roth IRAs have no required minimum distributions and withdrawals are completely tax-free. Leaving these untouched as long as possible allows them to grow and provides a powerful hedge against future tax rate increases.

How much can you safely withdraw each year

The 4% rule has been the starting point for this conversation for decades. The research behind it known as the Trinity Study found that a retiree who withdrew 4% of their portfolio in the first year of retirement and adjusted for inflation each year thereafter had a very high probability of not running out of money over a 30-year retirement, based on historical market returns.

It is a useful benchmark. But it is not a complete answer. Your safe withdrawal rate depends on your age at retirement, your portfolio allocation, your other income sources, your flexibility to reduce spending in a down market, and your goals for leaving assets to heirs. A 62-year-old with a 35-year retirement horizon should think about withdrawal rates differently than a 70-year-old who retired with a pension covering most of their expenses.

The most important thing the 4% rule gets right is this: your portfolio needs to be managed for growth, not just preservation. A retiree who keeps everything in cash or bonds out of fear will almost certainly outlive their money. Inflation alone erodes purchasing power in ways that only a growth-oriented portfolio can offset over a 25 to 30 year horizon.

The tax dimension of your retirement paycheck

One of the most common surprises new retirees encounter is how much of their retirement income is taxable. If most of your savings are in traditional 401(k)s and IRAs, every dollar you withdraw is taxed as ordinary income. Add Social Security benefits, up to 85% of which can become taxable depending on your combined income, and Medicare premium surcharges that kick in at higher income levels, and the effective tax burden in retirement can feel uncomfortably familiar to your working years.

This is why tax diversification across account types traditional, Roth, and taxable is so valuable going into retirement. Having the flexibility to choose where your income comes from in any given year gives you meaningful control over your tax bracket. In a year when your spending is higher, you draw more from Roth. In a year when you have room in a lower bracket, you take more from your traditional IRA and reduce future required minimum distributions. That kind of flexibility compounds in value over a long retirement.

The retirees who build the most efficient income streams are almost never the ones who saved the most. They are the ones who paid attention to which bucket every dollar came from.

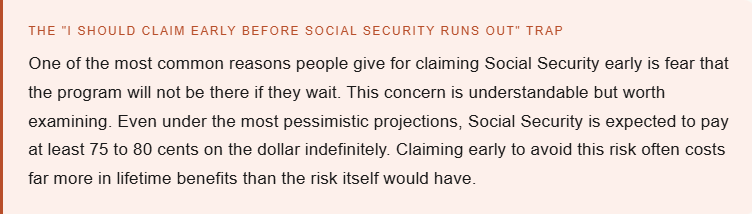

Social Security timing is a bigger decision than most people realize

Because Social Security forms the guaranteed foundation of most retirement income plans, the decision of when to claim deserves its own conversation. Claiming at 62 gives you income sooner but permanently reduces your monthly benefit by as much as 30% compared to your full retirement age. Waiting until 70 gives you the maximum possible benefit, with an 8% increase for every year you delay past full retirement age.

For a married couple, the optimal claiming strategy is even more nuanced. The higher earner delaying as long as possible protects the surviving spouse, who will inherit the larger of the two benefits for the rest of their life. That survivor benefit consideration alone changes the math for many couples who would otherwise both claim early.

Building your retirement paycheck plan

Putting this all together requires coordinating more moving pieces than most people realize going into retirement. The good news is that once the plan is built, it does not require constant attention. It requires an annual review, the discipline to follow a withdrawal sequence even when markets make that feel uncomfortable, and a willingness to adjust when life changes.

What a complete retirement income plan addresses

- Total guaranteed income from Social Security, pensions and annuities

- Monthly income gap that your portfolio needs to fill

- Withdrawal sequence across taxable, traditional and Roth accounts

- Safe withdrawal rate calibrated to your specific timeline and flexibility

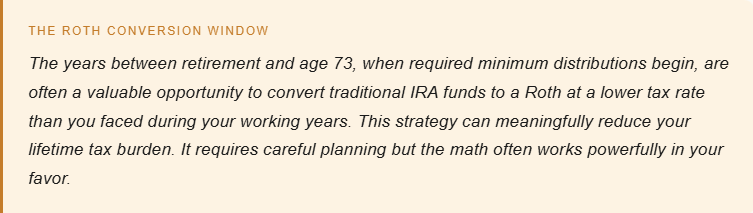

- Roth conversion strategy in the years before required minimum distributions begin

- Social Security claiming strategy, especially for married couples

- Tax bracket management across all income sources each year

- A healthcare and long-term care funding strategy

- An estate plan that reflects how you want remaining assets to transfer

None of this is beyond reach. But it does require intentional planning rather than improvisation. The retirees who feel most confident about their financial lives are almost universally the ones who went into retirement with a written income plan, not just a savings balance and a hope that it would be enough.